Clear Prop #12 | Blackbird Launch, Vectored-Thrust Dominant Design, eSTOL vs eVTOL

FEATURE: A Performance Comparison of eSTOL and eVTOL Aircraft

After a few months of hiatus, I am finally back to writing Clear Prop, your leading newsletter on all things related to Advanced Air Mobility research & venture strategy. In the last 6 months, I was busy launching my own advisory firm, Blackbird. Blackbird was founded with the burning passion for answering the following questions:

Given how difficult it is to raise venture capital, especially today, how can I personally support founders in raising capital swiftly and the “right way”?

How can I support startups maximize their returns as they land their first large contracts?

What do aerospace and in general, deep tech startups, need to do differently than CAPEX-light companies to successfully thrive and generate large venture outcomes?

The answer to all of these culminate in Blackbird, co-founded with my partner Maxim Matias. We are an early-stage advisory working with aerospace and deep tech firms on 1) Go-to-Market Strategy, 2) Business-Focused Quantitative Modelling, and 3) Capital-Raising. Our sweet spot is Pre-Seed to Series A and so far we have worked with 3 startups, raising together $2.5M in aggregate. Our primary success metric is the number of founders who have an exceptional product and a solid team, successfully 1) acquiring business contracts and 2) closing venture rounds.

If you have a startup or about to found one, get in touch with us. We are excited to engage early on to work with you in making your vision a success.

With this, let’s dive into this week’s venture strategy and research paper.

Lately, the topic of a dominant product design has been creating waves in the AAM community. A column published by the Aviation Week summarizes this well, touching on my talk that I had the pleasure giving at the VFS Transformative Vertical Flight in Santa Clara back in February.

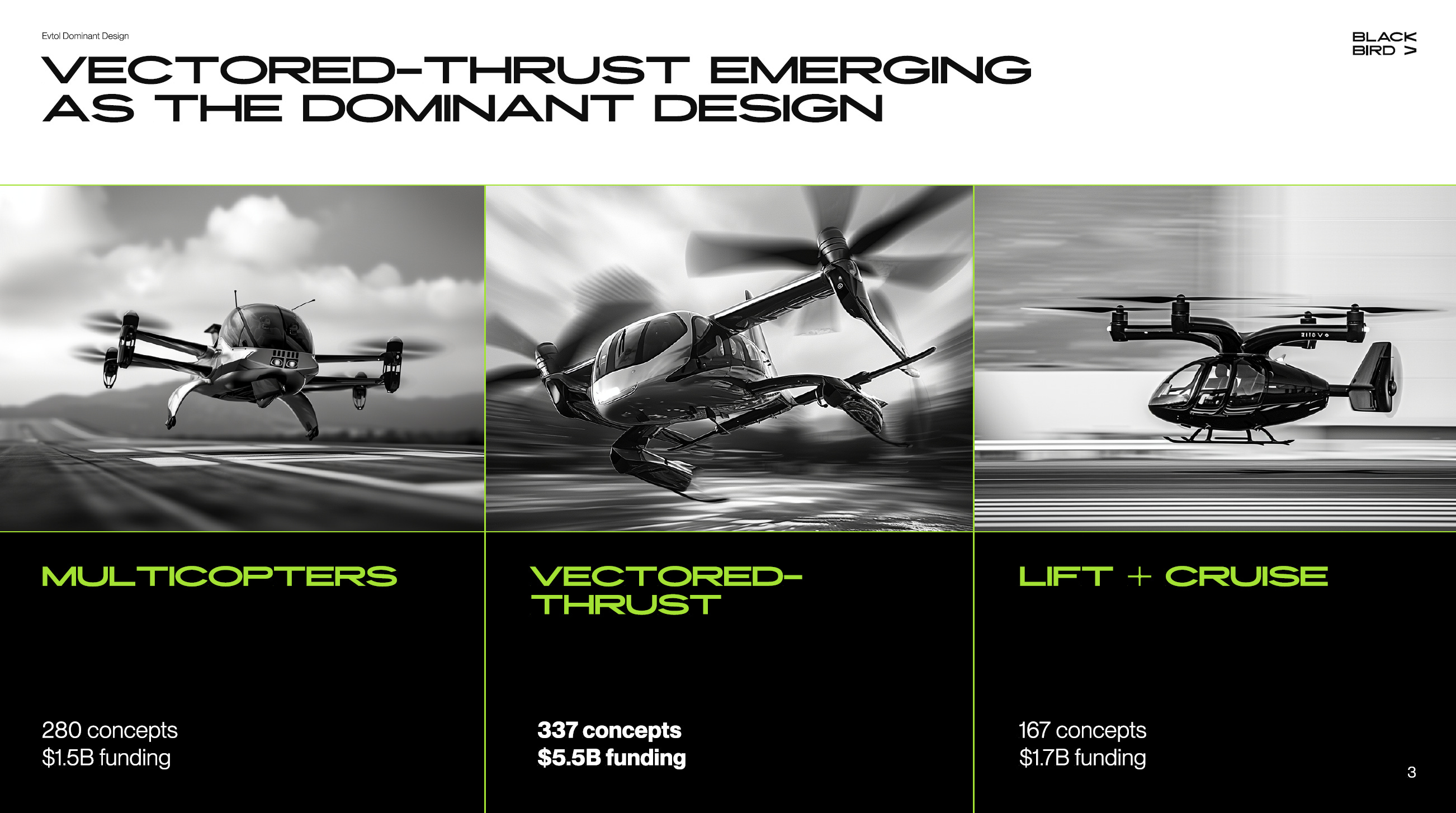

The gist is, there is a clear trend that the vectored-thrust configuration is emerging as the dominant design in passenger eVTOL.

There are a few signals that are important here. Let’s dive in:

1. Investment Concentration

Vectored-thrust eVTOLs - the tilt-rotors, tilt-wings, and the tilt-fans of the world - have garnered the most venture investment of all configurations. A total of $5.5Bn has gone into these firms so far (65% of all eVTOL funding), with the majority of it concentrated across 5 public firms. There is clear capital conviction on the vectored-thrust overall, which can be a significant force in determining which designs ultimately achieve commercial success.

In the last 18 months, subsequent to the COVID-fueled funding craze that generated the majority of investment into eVTOL through SPACs, investor interest has cooled off. Only the OEMs that can demonstrate the most certification and flight testing track record are able to attract investment. This means the firms that are most funded today, which the majority are vectored-thrust, will attract whatever major capital is available going forward.

(The other side of this coin is that if your eVTOL firm has had 100s of millions of $US of investment or more, you will be more likely to stick to the design that you have started with. The reason for this is simple. Path dependence. Simply put, the specific technical & commercial path you take as a company given significant capital investment will be a huge force upon you to keep going forward on that same path. Going back to the initial stages of conceptual design, pivoting into another eVTOL configuration will be a large sunk cost to you. Hence, the inertia caused by path dependence.)

2. Design Pivots by OEMs

The design space has seen multiple pivots into the vectored-thrust recently, specifically the tilt-rotor. Notable examples are Wisk, settling on a tilt-rotor design for their 6th-gen vehicle, and Vertical Aerospace, iterating through multicopters and finally freezing their product design as a tilt-rotor. In aggregate, 6 pivots into vectored-thrust represent more than $900M in venture funding.

Not only are there design pivots into the vectored-thrust but tilt-rotor designs between firms are also converging. The most prominent example that drew a lot of attention is the latest iteration of Hyundai’s (Supernal) eVTOL, which looks exceptionally similar to the Archer eVTOL. Therefore, designs are not only converging between OEMs that have different configurations, but also between those that have already settled into the vectored-thrust.

3. Regulatory Lock-in

So far, three G-1 certification papers by the FAA have been issued, and all of them have been to firms with vectored-thrust designs (namely Joby, Archer, and Lilium). With every G-1 paper, it becomes strategically more attractive to any new entrant to opt for the vectored-thrust design as the certification risk is lowered each time, compared to the lift+cruise and multicopters. For instance, if you are a startup that is just entering this space or a later-stage firm that hasn’t frozen their design configuration yet, you will be tempted to choose a design that has the most progress with the FAA.

This regulatory “lock-in” can add to the momentum behind the vectored-thrust emerging as the dominant design for pax eVTOL.

Now, why should we care that one design is emerging as dominant over all others?

There are multiple strong reasons to, whether you are an engineer, entrepreneur, corporation, or a researcher. For entrepreneurs, founding a venture as the dominant design is emerging is a window of opportunity that is correlated with success. This is because complexity is being de-risked in the ecosystem and conceptual thinking around the technology & use cases is solidifying.

Does this mean you should be founding a vehicle OEM startup? Not necessarily. Finding capital for building an eVTOL vehicle is incredibly difficult today, given investor fatigue post-COVID boom. The opportunity lies in providing solutions to the AAM ecosystem. These could be batteries, operations software, computer vision, advanced manufacturing, reliable comms, & many more.

On the other hand, large aerospace & automotive corporates can take advantage of this by repurposing their commercial strategy, perhaps pivoting their designs into the vectored-thrust or targeting unexplored use cases with totally different technical approaches.

Thirdly, for researchers and engineers, R&D and technical efforts can either be focused on 1) catering to the vectored-thrust or 2) going after niche use cases (and thus niche design configurations) that the center of the market isn’t building. This can increase the amount of technical output that is eventually commercialized and brought back to society in value dividends.

Being aware of the trends in the design space, it is a great time to build products in aerospace and time it correctly for large venture outcomes.

Keep on building & go get it!

A Performance Comparison of eSTOL and eVTOL Aircraft

Thinking about dominant designs, the electric short takeoff and landing (eSTOL) vehicle may turn out to be a viable option (and perhaps the dominant design!) for ranges and payloads currently not accessible to eVTOL. Envisioned to be operated from similarly constrained urban spaces such as rooftops, barges, ports, and heliports, but as a fixed-wing airplane, the eSTOL with its longer range could address the market for longer regional routes up to 500 mi such as Boston to DC or Barcelona to Geneva. Or perhaps shorter but demanded ones such as Gatwick to Luton Airport. This paper by MIT undertakes a comparison between eSTOL and eVTOL aircraft - covering battery- and hybrid-electric propulsion systems - weighing the tradeoffs of each configuration for a specific mission. Sizing studies of a tilt-rotor (think Archer!), tilt-duct (think Lilium!), and blown-lift (think Electra!) aircraft are conducted with a particular focus on payload, range, propulsion type, ground footprint constraints & vehicle geometry.

Key takeaways:

A battery-electric eSTOL aircraft can carry 1.9-2.2x the payload of an eVTOL for the same MTOW (maximum takeoff weight), range and speed while being able to operate from a 300-ft runway (a bit shorter than the length of a soccer field).

A hybrid-electric powertrain outperforms all-electric powertrains. A hybrid-electric eSTOL can carry the same payload 10x further at the same speed and altitude than an all-electric eSTOL at the same MTOW.

Comparing a hybrid-electric eSTOL and eVTOL, the former has a 1.8x increase in payload capability over the latter.

The performance benefit reaped from an eSTOL is diminished as the takeoff and landing location is made smaller. The cut-off for this is somewhere between 50-75 ft of runway length, below which eVTOLs are competitive.

For the technically-savvy, the wing sizing for the eSTOL is primarily constrained by takeoff and landing, causing a lower CL (lift coefficient) for cruise. The eVTOL, on the other hand, sizes its wings optimized for cruise since takeoff and landing is achieved primarily without wings. This means that cruise efficiency and speed are optimized for the eVTOL whereas the eSTOL needs to fly higher to achieve efficient cruise.

The BFD: There are less than a handful of startups building eSTOL vehicles today, of which the most prominent is a company out of MIT called Electra Aero, funded by Lockheed Martin Ventures. It is a curious occurrence that there are no other venture-funded companies that are targeting regional air mobility use cases with a hybrid-electric, eSTOL aircraft. Even if we look at the wider hybrid-electric aviation space (check out Ampaire, Pipistrel, Airbus!), this sub-vertical of AAM draws much less attention compared to eVTOL, whereas eVTOL has been able to generate the most hype in the mind of the public and investors. However, the upside with eSTOL is that it potentially has a faster path to commercialization without necessitating novel aircraft certification schemes, but through, for example, FAR Part 23.

That being said, eSTOL definitely has challenges with precision landing in such tight urban configurations, which may prompt the FAA for closer scrutiny on top of this. On the other hand, industry consensus is that eVTOL will take a longer time to be certified, especially with the FAA’s 180-deg turn of dictating Part 21.17(b) certification as powered-lift aircraft, which does not have a civil precedence as of today.

This edition’s sponsor is Vertical Flight Society. VFS is an amazing resource that I use to access leading technical papers and workshop decks for my work. Whether you are an investor, engineer, researcher, or entrepreneur, becoming a VFS member can give you an asymmetric advantage in the AAM space.

Membership gives discounted access to more than 15,000 technical papers, presentations and articles. Learn more here.

Great work Pamir Sevincel! As discussed, slight points to make on strategy/investment:

"The opportunity lies in providing solutions to the AAM ecosystem. These could be batteries, operations software, computer vision, advanced manufacturing, reliable comms, & many more."

- Actually, as stated in my previous update with IONA, the marginal cost and complexity of integrating "enablers" are often very low so I wouldn't recommend an investment (talking about software solutions only here e.g. telecoms, etc.). There are some expectations of course, but an investment is about Finance so "risk assessment" with the risk/reward ratio. (1) the "reward" is less because you can sell short term to AAM but there is a glass ceiling with lower defensibility and well-funded competitors, so you'll be acquired for a "$10-30M" if you're lucky, and (2) the market is smaller because you capture less of the value added and - again in the case of most software - you can't expand with a vertical integration to capture more of the value over time.

If I make a start-up investment, I need to see a moonshot otherwise I'll bear the risks without the potential reward. This is why many VCs are not making any money. Strategy is everything.

"That being said, eSTOL definitely has challenges with precision landing in such tight urban configurations, which may prompt the FAA for closer scrutiny on top of this."

I agree with most of what you say on eSTOL, technically, but again I don't see it as a good market opportunity. (1) What is the use case? If I have a soccer field to take off and need to lift a lot, I can just drive a truck to the local airport/airfield and it will be much cheaper and energy-efficient. Either I want to use a super-efficient aircraft, CTOL, or I need a VTOL capability. A company doing an eSTOL would be in between, missing a lot of potential from both the CTOL and VTOL markets, yet bearing (again) the high risks of infrastructure adaptation, regulations etc. (2) there is often an overlook of "alternatives" when people consider these strategies: you're not competing with the AAM here, but with every other vehicle (road/maritime or airships) that may perform what you want to do with an eSTOL or eVTOL. This is also why I wouldn't invest in most Passenger eVTOL start-ups, and even less in an eSTOL one: the market is getting smaller and smaller as you consider all the autonomous mobility and future of mobility alternatives, and yet the valuations were high (despite down rounds now) so this is also not an investment I would make.

NB: I'm not that sure about the ease to certify an eSTOL by the way, as the interest would be to take off from suburban/urban areas where their incapacity to hover/requirement to generate lift should become a problem to demonstrate redundancy/safety.